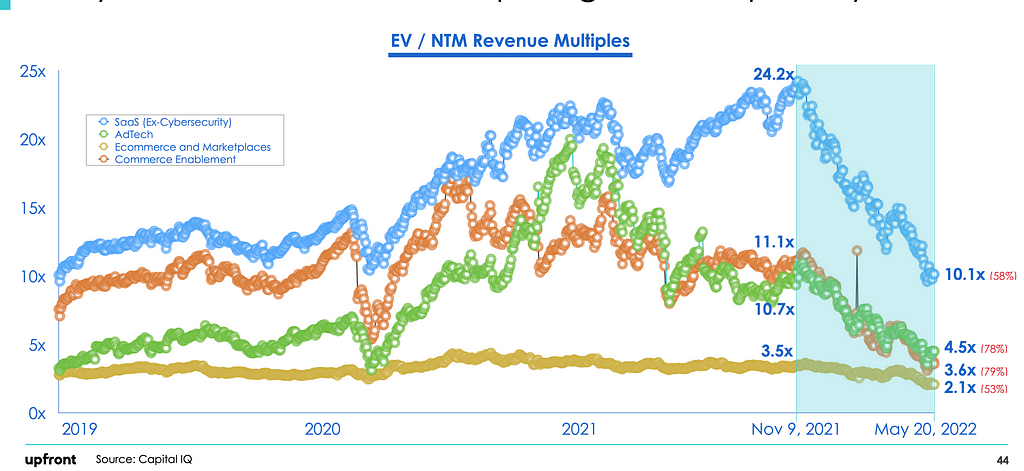

At our mid-year offsite our partnership at Upfront Ventures was discussing what the future of venture capital and the startup ecosystem looked like. From 2019 to May 2022, the market was down considerably with public valuations down 53–79% across the four sectors we were reviewing (it is since down even further).

==> Aside, we also have a NEW LA-based partner I’m thrilled to announce: Nick Kim. Please follow him & welcome him to Upfront!! <==

Our conclusion was that this isn’t a temporary blip that will swiftly trend-back up in a V-shaped recovery of valuations but rather represented a new normal on how the market will price these companies somewhat permanently. We drew this conclusion after a meeting we had with Morgan Stanley where they showed us historical 15 & 20 year valuation trends and we all discussed what we thought this meant.

Should SaaS companies trade at a 24x Enterprise Value (EV) to Next Twelve Month (NTM) Revenue multiple as they did in November 2021? Probably not and we think 10x (May 2022) seems more in line with the historical trend (actually 10x is still high).

What You Can Learn From Public Markets

It doesn’t really take a genius to realize that what happens in the public markets is highly likely to filter back to the private markets because the ultimate exit of these companies is either an IPO or an acquisition (often by a public company whose valuation is fixed daily by the market).

This happens slowly because while public markets trade daily and prices then adjust instantly, private markets don’t get reset until follow-on financing rounds happen which can take 6–24 months. Even then private market investors can paper over valuation changes by investing at the same price but with more structure so it’s hard to understand the “headline valuation.”

But we’re confident that valuations will get reset. First in late-stage tech companies and then it will filter back to Growth and then A and ultimately Seed Rounds.

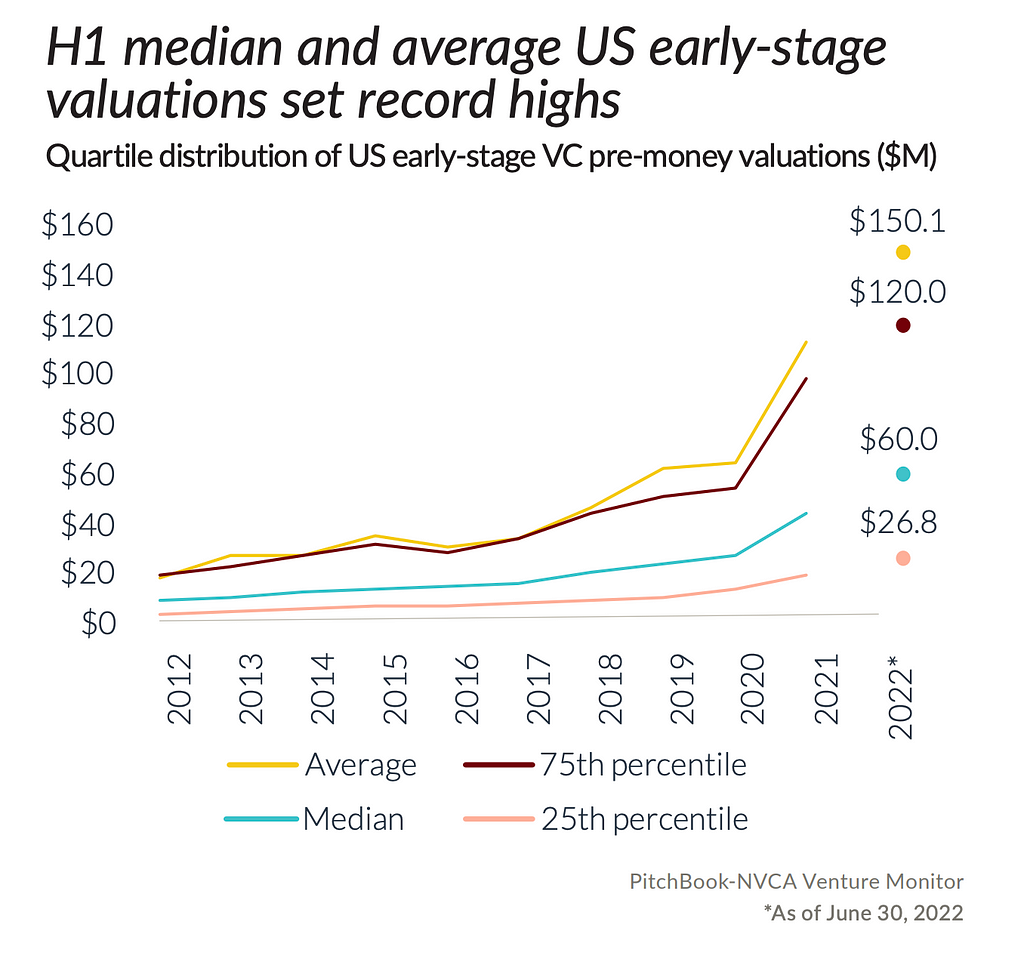

And reset they must. When you look at how much median valuations were driven up in the past 5 years alone it’s bananas. Median valuations for early-stage companies tripled from around $20m pre-money valuations to $60m with plenty of deals being prices above $100m. If you’re exiting into 24x EV/NTM valuation multiples you might overpay for an early-stage round, perhaps on the “greater fool theory” but if you believe that exit multiples have reached a new normal, it’s clear to me: YOU. SIMPLY. CAN’T. OVERPAY.

It’s just math.

No blog post about how Tiger is crushing everybody because it’s deploying all its capital in 1-year while “suckers” are investing over 3-years can change this reality. It’s easy to make IRRs work really well in a 12-year bull market but VCs have to make money in good markets and bad.

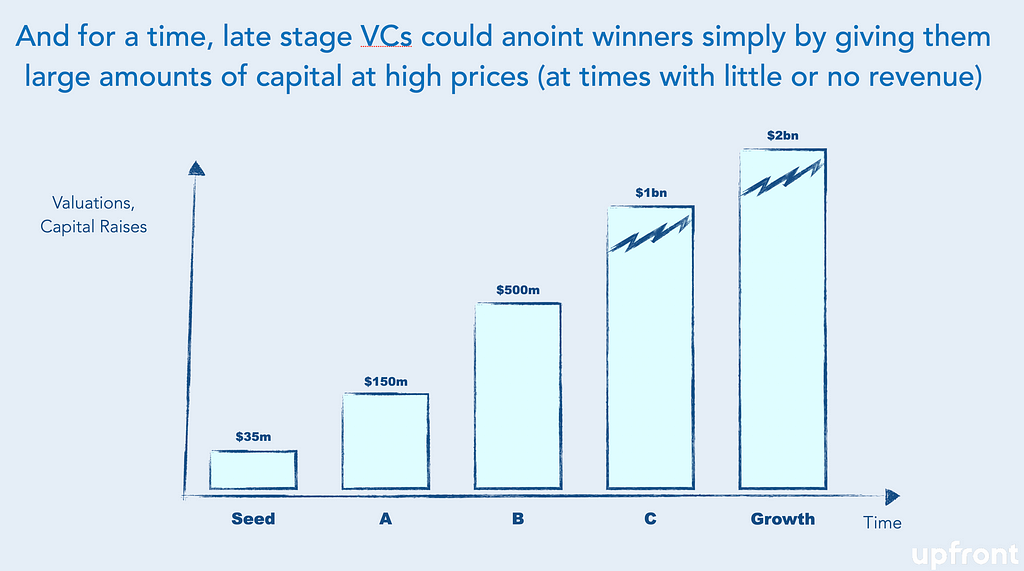

In the past 5 years some of the best investors in the country could simply anoint winners by giving them large amounts of capital at high prices and then the media hype machine would create awareness, talent would race to join the next perceived $10bn winner and if the music never stops then everybody is happy.

Except the music stopped.

What Happens Next?

There is a LOT of money still sitting on the sidelines waiting to be deployed. And it WILL be deployed, that’s what investors do.

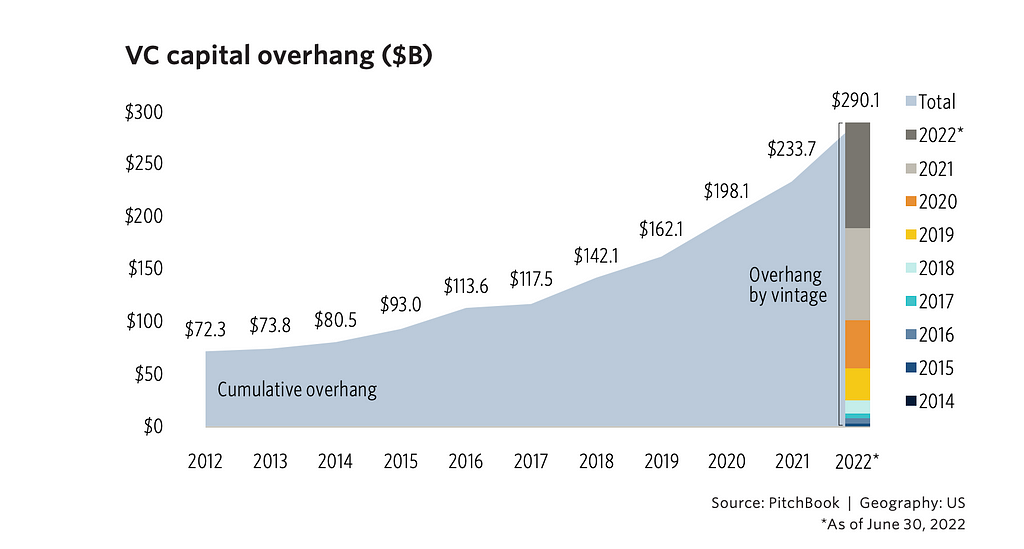

Pitchbook estimates that there is about $290 billion of VC “overhang” (money waiting to be deployed into tech startups) in the US alone and that’s up more than 4x in just the past decade. But I believe it will be patiently deployed, waiting for a cohort of founders who aren’t artificially clinging to 2021 valuation metrics.

I talked to a couple of friends of mine who are late-stage growth investors and they basically told me, “we’re just not taking any meetings with companies who raised their last growth round in 2021 because we know there is still a mismatch of expectations. We’ll just wait until companies that last raised in 2019 or 2020 come to market.”

I do already see a return of normalcy on the amount of time investors have to conduct due diligence and make sure there is not only a compelling business case but also good chemistry between the founders and investors.

What is a VC To Do?

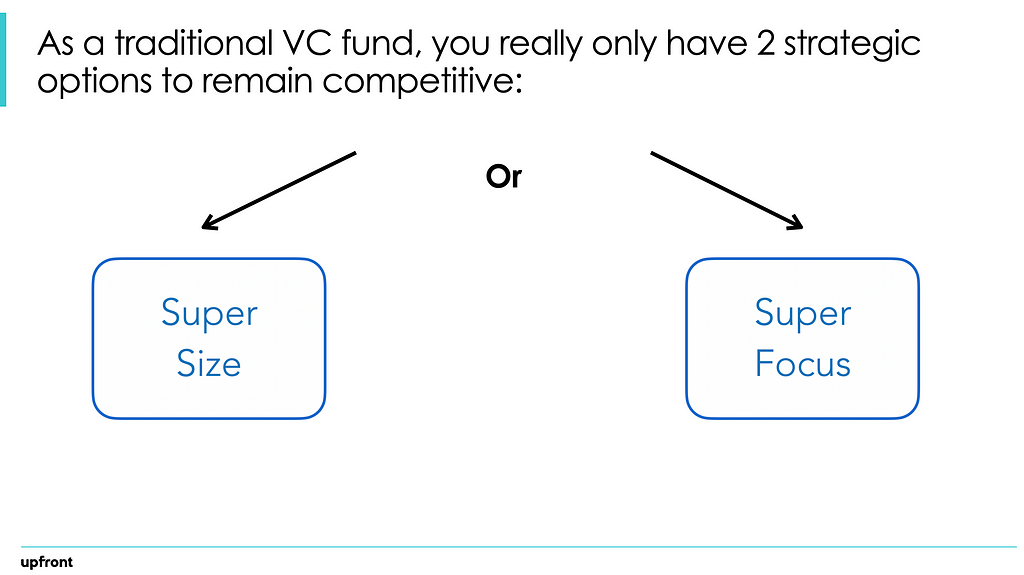

I can’t speak for every VC, obviously. But the way we see it is that in venture right now you have 2 choices — super size or super focus.

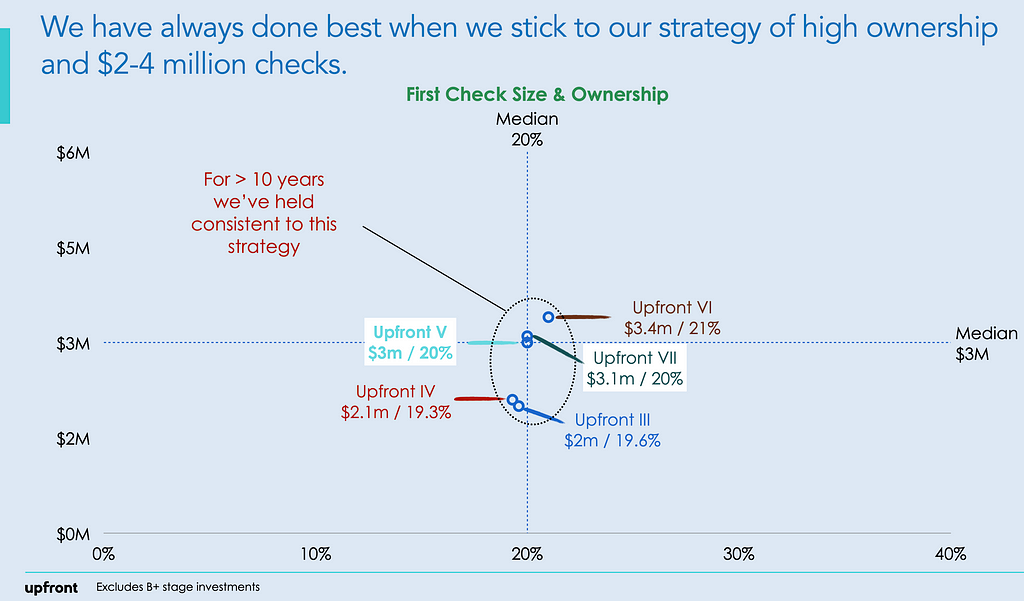

At Upfront we believe clearly in “super focus.” We don’t want to compete for the largest AUM (assets under management) with the biggest firms in a race to build the “Goldman Sachs of VC” but it’s clear that this strategy has had success for some. Across more than 10 years we have kept the median first check size of our Seed investments between $2–3.5 million, our Seed Funds mostly between $200–300 million and have delivered median ownerships of ~20% from the first check we write into a startup.

I have told this to people for years and some people can’t understand how we’ve been able to keep this strategy going through this bull market cycle and I tell people — discipline & focus. Of course our execution against the strategy has had to change but the strategy has remained constant.

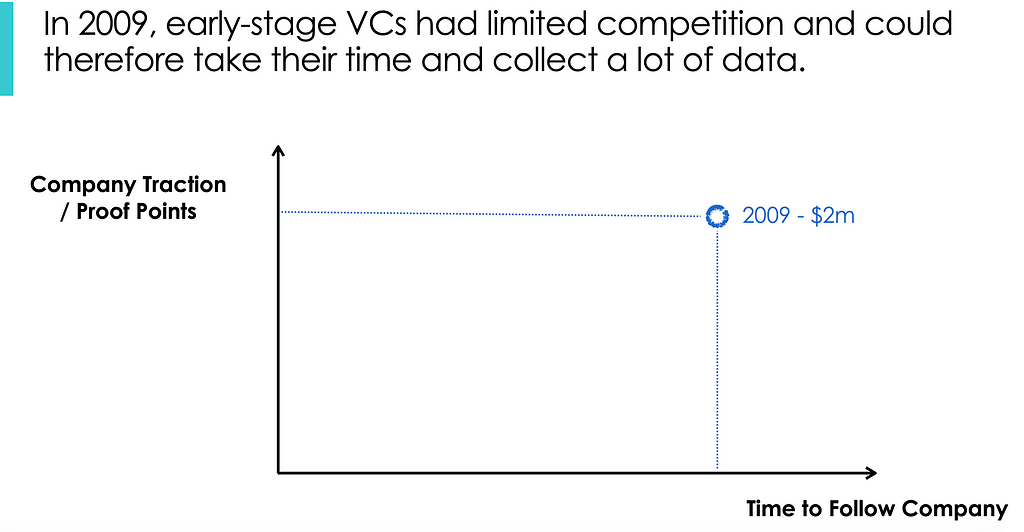

In 2009 we could take a long time to review a deal. We could talk with customers, meet the entire management team, review financial plans, review customer purchasing cohorts, evaluate the competition, etc.

By 2021 we had to write a $3.5m first check on average to get 20% ownership and we had much less time to do an evaluation. We often knew about the teams before they actually set up the company or left their employer. It forced extreme discipline to “stay in our swimming lanes” of knowledge and not just write checks into the latest trend. So we largely sat out fundings of NFTs or other areas where we didn’t feel like we were the expert or where the valuation metrics weren’t in line with our funding goals.

We believe that investors in any market need “edge” … knowing something (thesis) or somebody (access) better than almost any other investor. So we stayed close to our investment themes of: healthcare, fintech, computer vision, marketing technologies, video game infrastructure, sustainability and applied biology and we have partners that lead each practice area.

We also focus heavily on geographies. I think most people know we’re HQ’d in LA (Santa Monica to be exact) but we invest nationally and internationally. We have a team of 7 in San Francisco (a counter bet on our belief that the Bay Area is an amazing place.) Approximately 40% of our deals are done in Los Angeles but nearly all of our deals leverage the LA networks we have built for 25 years. We do deals in NYC, Paris, Seattle, Austin, San Francisco, London — but we give you the ++ of also having access in LA.

To that end I’m really excited to share that Nick Kim has joined Upfront as a Partner based out of our LA offices. While Nick will have a national remit (he lived in NYC for ~10 years) he is initially going to focus on increasing our hometown coverage. Nick is an alum of UC Berkeley and Wharton, worked at Warby Parker and then most recently at the venerable LA-based Seed Fund, Crosscut.

How Does the Industry Really Work?

Anybody who has studied the VC industry knows that it works by “power law” returns in which a few key deals return the majority of a fund. For Upfront Ventures, across > 25 years of investing in any given fund 5–8 investments will return more than 80% of all distributions and it’s generally out of 30–40 investments. So it’s about 20%.

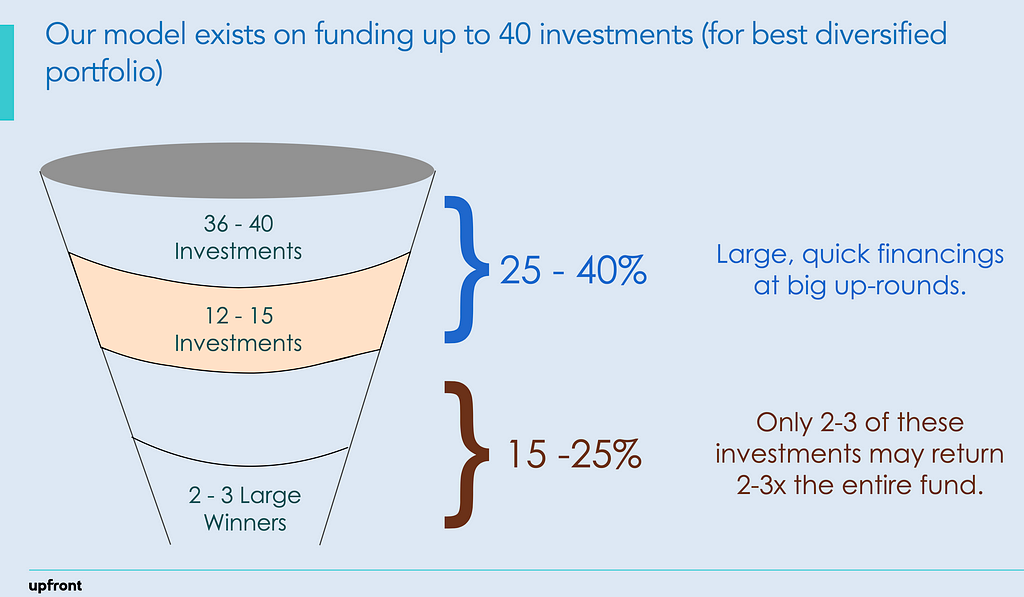

But I thought a better way of thinking about how we manage our portfolios is to think about it as a funnel. If we do 36–40 deals in a Seed Fund, somewhere between 25–40% would likely see big up-rounds within the first 12–24 months. This translates to about 12–15 investments.

Of these companies that become well financed we only need 15–25% of THOSE to pan out to return 2–3x the fund. But this is all driven on the assumption that we didn’t write a $20 million check out of the gate, that we didn’t pay a $100 million pre-money valuation and that we took a meaningful ownership stake by making a very early bet on founders and then partnering with them often for a decade or more.

But here’s the magic few people ever talk about …

We’ve created more than $1.5 billion in value to Upfront from just 6 deals that WERE NOT immediately up and to the right.

The beauty of these businesses that weren’t immediate momentum is that they didn’t raise as much capital (so neither we nor the founders had to take the extra dilution), they took the time to develop true IP that is hard to replicate, they often only attracted 1 or 2 strong competitors and we may deliver more value from this cohort than even our up-and-to-the-right companies. And since we’re still an owner in 5 out of these 6 businesses we think the upside could be much greater if we’re patient.

And we’re patient.

What Does the Post Crash VC Market Look Like? was originally published in Both Sides of the Table on Medium, where people are continuing the conversation by highlighting and responding to this story.

Source: Both Sides of the Table - Medium